Escalating premiums and deductibles have driven about 10,000 Mainers over a health care “cliff,” where they can barely afford coverage thanks to a vulnerability in the Affordable Care Act exploited by the actions of the Trump administration.

Depending on the plan chosen, premiums have increased by about 70 percent or more since 2014 for people who earn too much to qualify for subsidies for the federal health care program. By contrast, ACA enrollees with subsidies have been mostly shielded from rate increases. The lack of a cap on premium increases, or other cost controls, for ACA enrollees who earn more than 400 percent of the federal poverty limit leaves them unprotected, making the “affordable” part of the program for some impossible.

Those cost hikes have accelerated since President Trump took office, and ratepayers are expected to be pummeled with giant rate increases again in 2019. Rates haven’t yet been filed with the Maine Bureau of Insurance, but will be by May.

“The cliff is real,” said Erik Wengle, a research analyst with the Urban Institute, a Washington-based think tank. “These plans have gotten quite expensive, and as they’ve gotten more expensive, we’re seeing people getting priced out.”

People earning more than 400 percent of the federal poverty limit – about $81,000 for a family of three, $65,000 for a two-person family or $48,000 for a single person – are not eligible for subsidies in the ACA marketplace.

“These are people firmly in the middle class,” Wengle said.

COSTS VARY COUNTY BY COUNTY

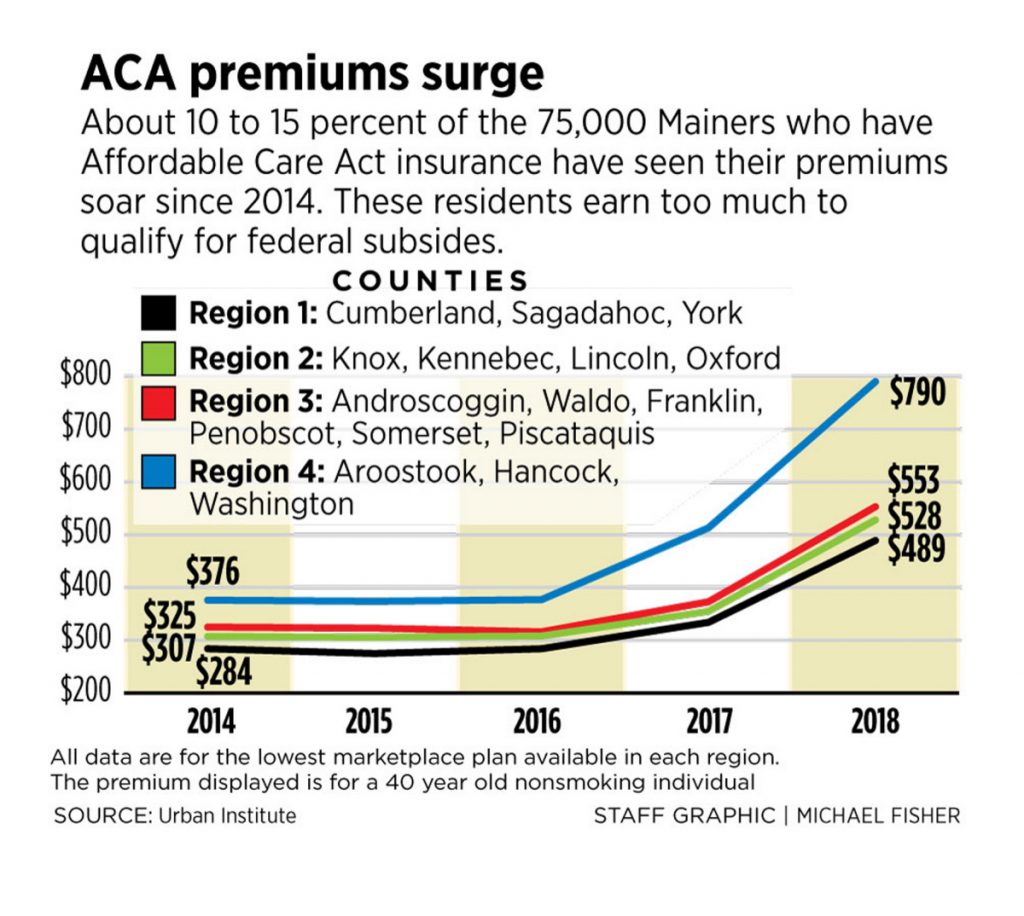

This subset – consistently about 10 to15 percent of the 75,000 Mainers who have ACA marketplace insurance – have seen their premiums soar. A 40-year-old single nonsmoker in Cumberland County who earns $50,000 per year has seen premiums for a silver plan increase from $284 per month in 2014 – the first year the ACA marketplace was in effect – to $489 in 2018, a 72 percent increase. If that same person lived in Aroostook County, he or she would have seen premiums increase from $376 per month to $790 per month, a 110 percent hike, according to an Urban Institute analysis.

Meanwhile, those who qualify for the subsidies are mostly protected from premium increases, because the subsidies go up roughly the same amount that premiums increase. For example, some silver plans in 2018 cost about $300 to $350 for those just under 400 percent of the poverty level, while bronze plans can be purchased for about $75 to $150, depending on where in Maine you live.

For those who don’t qualify for subsidies, they shoulder the entire burden of the increases.

Eric Cioppa, Maine Bureau of Insurance superintendent, said the state intends to start a reinsurance program for 2019 that will help keep insurance premiums in check, but affording insurance will still be difficult, especially for those who make more than 400 percent of poverty level.

“It’s literally becoming unaffordable if you’re over 400 percent,” Cioppa said.

The ACA categorizes its plans as bronze, silver or gold, with bronze having the lowest premiums but high deductibles; gold offering generous benefits, higher premiums and lower deductibles; and silver plans falling in the middle.

COUPLE ADVISED TO EARN LESS

For the Rices of Durham and the Williamses in Stonington, both empty-nester families that earn more than 400 percent of the poverty limit, going over the affordability cliff means sky-high deductibles and premiums.

“I have to bite my tongue when people complain about a $20 premium increase. I feel like saying, ‘Are you kidding me? Let me show you what I pay,’ ” said Jane Rice, a financial adviser who owns a Christmas tree farm with her husband, David, 60.

Rice, 57, said her husband has previously had prostate cancer and currently is being treated for esophageal cancer, and they expect to hit the out-of-pocket maximum, which this year is about $25,000, including premiums and deductibles.

Their total premiums are $1,500 per month with an $11,000 deductible.

Both are self-employed small-business owners who don’t have access to employer-based insurance – one of the key categories of people the ACA was designed to help. And for business owners who make less than 400 percent of the poverty level, it has kept insurance relatively affordable. But those who earn more have increasingly had to pay more.

Rice said she’s been told a few times that they “need to make less money.” The cliff effect creates a reverse incentive, because health care costs increase dramatically once enrollees earn slightly more than 400 percent of the poverty level.

“I reject that. I want to be successful and for our businesses to be successful,” Rice said.

She declined to list their family income, but she said the only way they’ve been able to afford insurance is by being frugal.

“We live within our means and we are hard-working people,” Rice said. “Sometimes it feels like we are paying the equivalent of insurance for six people, not two. It has just been ridiculous. It is just not right.”

Judy and John Williams of Stonington said they earn about $100,000 but they’ve also seen the cost of health insurance jump to nearly unaffordable levels. But as a couple nearing retirement age, they value insurance and know they need it, even though they’ve been generally healthy. As lobstermen, the couple don’t have access to employer-based insurance.

Ann Woloson of health advocacy group Consumers for Affordable Health Care says “we are creating a sicker, more expensive health insurance marketplace” when young people have little incentive to get coverage and people like John and Judy Williams, above, subsidize care for everyone else. Staff photo by Gregory Rec

John is 63 and Judy is 62, and they pay a combined premium of $1,997. Their deductible was $750 four years ago, but now it’s $5,400.

“We have to spend nearly $12,000 before the insurance kicks in,” John Williams said. “We’re very fortunate that we can pay the premiums, but it’s a lot of money.”

He said that they are looking forward to age 65 when Medicare kicks in and coverage is free, although many often purchase “gap insurance” to pay for things that insurance doesn’t cover. But he said he doesn’t mind knowing that people who earn less can get insurance for far less.

People earning up to about $27,000 in Maine can qualify for zero-premium bronze plans through the ACA, while typical premiums for people who earn about $40,000 to $45,000 are about $200 to $300 per month, depending on age and where you live. Insurers can charge up to three times more based on age, and can charge more based on address.

Williams said the disparity is unfortunate, but doesn’t change his opinion that insurance should be affordable. He said it doesn’t bother him that some at lower incomes have access to zero-premium insurance while he and Judy have expensive insurance.

“People that need insurance should be allowed to have it. Everyone should be able to afford insurance,” Williams said.

ACA FIXES HAVEN’T BEEN ENACTED

The Trump administration in 2017 ended cost-sharing reduction payments to insurance companies – payments that were designed to help lower-income people afford out-of-pocket costs such as co-pays and deductibles. Ending the cost-sharing reduction payments had no effect on lower-income people, but increased premiums for people earning more than 400 percent and skewed the market. To prevent further weakening of the ACA marketplace, state insurance commissioners, including in Maine, responded with complicated work-arounds that resulted in zero-premium bronze plans and lower-cost gold plans that were much better deals than in previous years.

The ACA, as former President Barack Obama’s signature domestic policy achievement, has been caught up in partisan politics almost since it was signed into law in March 2010. Trump campaigned against it, and has vowed to get rid of it.

Most Republicans in Congress agreed with Trump, while Democrats have stood behind it and worked with a few moderate Republicans, including Maine Sen. Susan Collins, to save the law.

In 2017, Congress attempted to repeal the ACA, but those efforts failed by one vote in the Senate, with Collins one of three senators to buck the party and vote to preserve Obamacare. But in a year-end party-line vote, Collins sided with Republicans on a tax cut package that included repealing the Affordable Care Act’s individual mandate. Collins supported the tax bill in exchange for Republican leadership promises to pass ACA stabilization measures, but those efforts collapsed last month.

Repealing the individual mandate – which requires people to purchase insurance or pay a penalty – makes it more likely that young, healthy people will not purchase insurance, driving up costs, according to health care experts.

Ann Woloson, executive director of Consumers for Affordable Health Care, an Augusta-based health advocacy group, said the cost of insurance for those making more than 400 percent of the poverty limit prices people out if they have any kind of significant debt – such as car payments, mortgages and other loans.

“It is unaffordable and unsustainable for people,” Woloson said. “We are creating a sicker, more expensive health insurance marketplace.”

One of the fixes touted by Collins – a federal plan to direct $30 billion over three years for reinsurance – would have helped keep premiums in check for people above the subsidy threshold. But it was paired with another reform – restoring the cost-sharing reduction payments – that received a mixed review in a Congressional Budget Office report released last week.

The work-arounds created by states lowered premiums for many, so unwinding those work-arounds when restoring the insurance company payments would cause many earning less than 400 percent to experience premium increases. The mixed CBO report and a fight over Obamacare abortion restrictions supported by Republicans deep-sixed the deal.

Democrats have since launched a counterplan that would, among other things, cap costs for those making more than 400 percent of poverty level to 8.5 percent of their income. With Republicans in control of Congress, it’s not likely to go anywhere, at least this year.

Woloson said the ACA is still standing and helping about 20 million Americans, through Medicaid expansion and ACA coverage. Maine voters approved Medicaid expansion in November but Republican Gov. Paul LePage is fighting Democrats in the State House over implementation costs.

‘ESSENTIAL’ BENEFITS NOT COVERED

Complicating the health care picture is a state-run reinsurance program that was put on hold when the ACA started. A LePage-era reform, it is likely to be relaunched and take effect in 2019.

The state’s reinsurance plan – called the Maine Guaranteed Access Reinsurance Association – redistributes insurance money by charging a fee of $4 per person per month on individual, small and large group plans, and funneling the revenue only to individual plans. The plan would also tap into federal money to help pay for what is estimated to be a $90 million program in 2019, according to Milliman, an insurance consultancy firm. That will help keep premiums 10 percent lower than they otherwise would be, but since rates haven’t been filed yet, Cioppa, the Maine Bureau of Insurance superintendent, said it’s unknown what the rate hikes will be for 2019.

The Trump administration is also promoting the expansion of short-term and association plans that would further undermine the ACA markets, Woloson said. Those short-term and association plans would be exempt from “essential health benefits” that all ACA plans are required to cover, such as maternity care, mental health, prescription drugs and substance use treatment. While they would carry lower premiums, Woloson said, patients would often find that many services aren’t covered, which was often the case with individual plans purchased prior to passage of the ACA. Often these plans were called “junk insurance” and if allowed to flourish would further weaken the ACA and could cause premium spikes, Woloson said.

The Trump administration has indicated that the association and short-term plans are on the way, but they are still going through federal rule-making.

Kevin Lewis, chief executive officer of Community Health Options, a nonprofit that provides ACA insurance, said what will happen with short-term and association plans is a “big looming question” of “paramount importance.”

Cioppa said Maine law currently allows for “rigorous” regulation of short-term and association plans. As long as the federal government doesn’t try to usurp state authority to regulate those plans, Cioppa said that Maine will be able to prevent them from weakening the ACA marketplace.

In addition to the 10,000 who have ACA marketplace plans and earn more than 400 percent of the federal poverty limit, an additional 9,000 people have off-marketplace plans, and many of them also would not qualify for subsidies.

Meanwhile, John Williams, the Stonington lobsterman, said the system needs an overhaul.

“All I know is, there’s got to be a better way of doing this than what we’re doing now,” Williams said.

Joe Lawlor can be contacted at 791-6376 or at:

Twitter: joelawlorph

Comments are no longer available on this story