Investors are taking interest in a Maine startup that promises to use technology to teach financial responsibility to kids.

York-based online youth banking app developer Ourly recently received a $3.4 million round of investment from a group of angel investors led by BlueIO, a Boston venture capital firm. Ourly has developed an online service that allows parents to automatically compensate their children for performing various tasks such as completing chores or achieving good grades. The company offers the app as a standalone product and also seeks to license its technology to banks and credit unions.

There are a variety of youth money-management apps on the market such as Bankaroo, iAllowance and PiggyBot. What’s different about the Ourly app is that it is designed to be integrated with financial institutions’ existing online banking platforms, said Mike Vien, the company’s CEO.

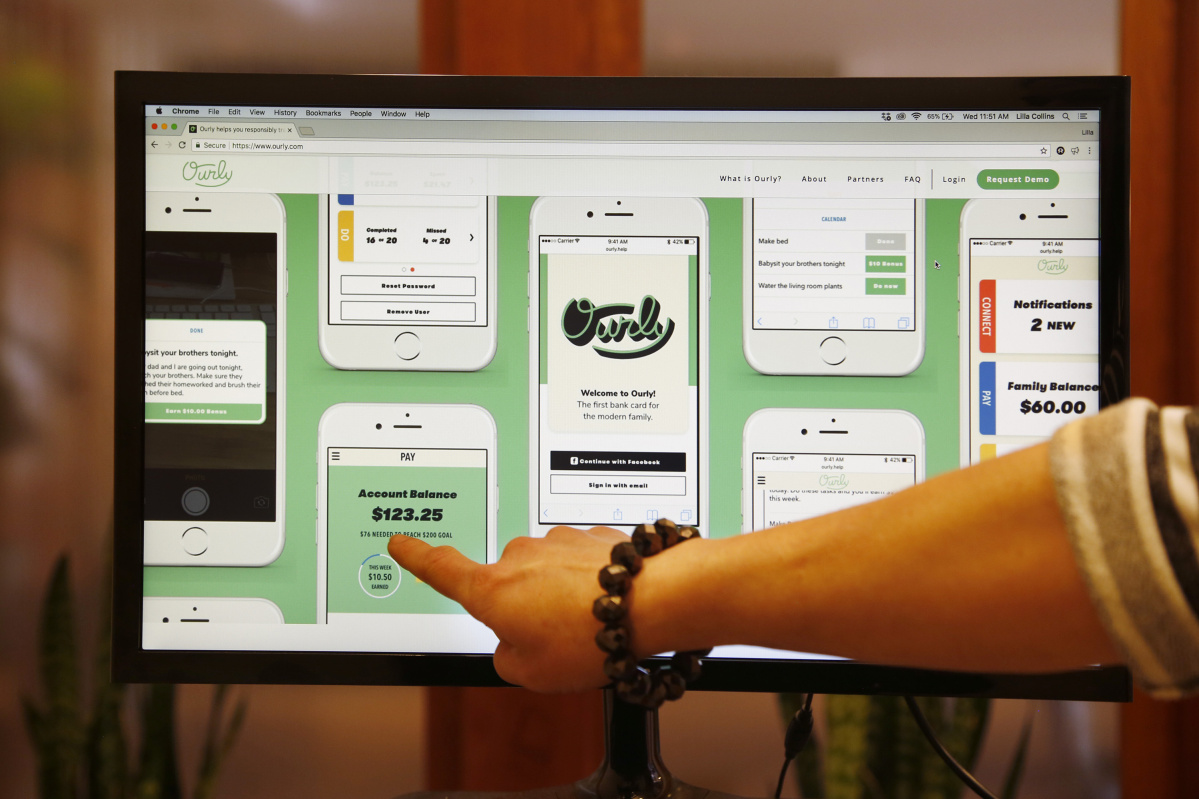

A variety of cellphone apps for a kids’ banking platform developed by Ourly is pointed out on a computer screen Wednesday.

Ourly is working on partnership agreements with banks and credit unions that would allow them to offer the company’s youth banking platform to customers under their own branding as an added service, he said. A few financial institutions already have signed up, Vien said, and several others are in negotiations.

“What parents kept telling us is that they wanted (an app that’s connected to) a real bank account,” he said.

Ourly customer Keith Ablow of Newbury, Massachusetts, said the app is easy for parents and children to use. Ablow signed up about a year ago to use the app with his son Cole, who is 16.

“It’s allowed my son to automate his allowance, if you will,” Ablow said. “It’s the kind of thing that removes any debate from the equation.”

Once a family registers to use the free service on Ourly’s website, the parents can assign specific tasks for their kids to complete and set a monetary value for each task. The money is pre-loaded by the parents into the app, to be released to the kids when the tasks are completed.

Once a task is completed, the child uploads a photo to the app as proof, such as a mowed lawn, a cleaned room or a completed homework assignment. The parents view the picture, approve it, and the money is transferred to the child, either as an electronic bank deposit or a digital gift card.

Ablow said that like most kids, his son is constantly engaged with information technology. As a result, the Ourly app is a natural way for him to deal with things like chores and allowances.

“It meets teenagers where they work and play,” he said. “I find it tremendously useful.”

Vien said financial institutions are always looking for ways to get younger consumers more comfortable with banking, and that Ourly is a good way to do it. He noted that millennials in particular have expressed an aversion to banks in surveys.

“Seventy-one percent of millennials said they would rather go to the dentist than listen to banks,” Vien said.

He also noted that young people represent a significant slice of the U.S. economy. Vien said the under-30 set, despite many of them not being old enough to drive, vote or work full time, actually control about $200 billion in annual direct spending when factoring in all income sources such as allowances, part-time jobs, babysitting, yardwork and gifts received for birthdays and holidays.

Todd Mason, president and CEO of the Maine Credit Union League, said he sees value in any technology that promotes financial literacy.

“There is a big need for youth financial education and services,” Mason said. “We love to see innovation in this area. It is great to see other organizations that share the same passion credit unions have for serving our youth, especially with technology.”

Chris Pinkham, CEO of the Maine Bankers Association, said he supports the type of service Ourly is proposing, although he bristled at the company’s contention that young people hate banks. Pinkham said as long as Ourly can comply with the banking industry’s strict regulatory standards, he thinks financial institutions will be interested in signing up.

“It’s really a great concept, and supporting financial literacy is a high priority for all banks, because that’s the future customer base,” he said.

Ablow said one thing he appreciates about the Ourly app is that unlike a lot of today’s techology, it is rooted in real-world tasks and reinforces the value of doing actual work.

“It builds self-esteem and it builds a work ethic,” he said.

J. Craig Anderson can be contacted at 791-6390 or at:

Twitter: @jcraiganderson

Comments are no longer available on this story